Binance Historical Data

Binance is one of the largest cryptocurrency exchanges in terms of daily crypto trading volume. It was founded in 2017 by Changpeng Zhao, a developer who had previously created high frequency trading software. Binance supports hundreds of the most commonly traded cryptos and tokens, including bitcoin (BTC), ether (ETH), litecoin (LTC), dogecoin (DOGE), and its own coin, BNB.

Like other crypto exchanges, Binance offers trading, listing, fundraising, de-listing, and withdrawing cryptocurrencies. It has a separate platform for U.S. residents called Binance.US, which allows users to buy, sell, and trade cryptocurrencies and altcoins with some of the lowest fees in the market.

Amberdata’s Binance Crypto Market Data Features

We offer:

- Binance spot data from 2017-08-17, and Binance.US spot data from 2019-09-17.

- Binance futures data from 2019-09-08.

- Historical tickers, tick-by-tick data, order book events, order book snapshots, reference quotes, OHLCV/candlesticks, prices, trades, VWAP and TWAP.

- Thousands of trading pairs.

- Binance live and historical futures and perpetuals, including open interest, long-short ratios, order books, liquidations, funding rates, insurance funds.

- All of this is downloadable by CSV through API docs.

- We capture data that Binance itself does not store.

- Our data formats are REST API and Futures in AWS S3

Our Data:

Trades: Our trade datasets consist of all tick-by-tick trade data, timestamped, and with the trade direction normalized from the taker side. Our Trade endpoints provide historical (time series) trade data for the specified pair or instrument.

Order books: Order Book Snapshots, we collect via the exchanges REST API and the snapshot is a one-minute snapshot. Every minute we get the full order book, full depth, from the exchange (as much as they provide).

OHLCV: OHLCV is an aggregated form of market data standing for Open, High, Low, Close and Volume. OHLCV data includes 5 data points: the Open and Close represent the first and the last price level during a specified interval; High and Low represent the highest and lowest reached price during that interval; Volume is the total amount traded during that period. This data is most frequently represented in a candlestick chart, which allows traders to perform technical analysis on intraday values.

VWAP: The volume-weighted average price (VWAP) is a measurement that shows the average price of an asset, adjusted for its volume over a given period of time. VWAP gives traders a smoothed-out indication of an asset’s price (adjusted for volume) over a given period of time.

Tickers: Tickers represent the best bids/asks from an order book. The bid price represents the maximum price that a buyer is willing to pay for an asset. The ask price represents the minimum price that a seller is willing to take for that same asset.

Binance Historical Trade Data

Our Binance trade datasets consist of all tick-by-tick trade data, timestamped, and with the trade direction normalized from the taker side. We have Binance spot data from 2017-08-17 and Binance.US spot data from 2019-09-17. We provide historical trade data via our REST API and real-time trade data via WebSockets for every single asset on Binance. We collect trade data by connecting to Binance’s REST API’s. We poll their market data REST API made publicly available in our API documentation.

We collect every executed transaction, and we poll at regular intervals to ensure that we are collecting every trade data point. Immediately after receiving these trades, we normalize the data into our own schema, to ensure consistency across exchanges. Our Binance trade history can be downloaded in CSV files or accessed through a REST API.

Our Trade endpoints provide historical (time series) trade data for the specified pair or instrument. The data is available via REST API and is limited to 60 API requests per second.

Binance Trade Data API Endpoitns

Spot

/market/spot/trades/information

/market/spot/trades/{pair}/historical

Futures

/market/futures/trades/information

/market/futures/trades/{instrument}/historical

Options

/market/options/trades/information

/market/options/trades/{instrument}/historical

Swaps

/market/swaps/trades/information

/market/swaps/trades/{instrument}/historical

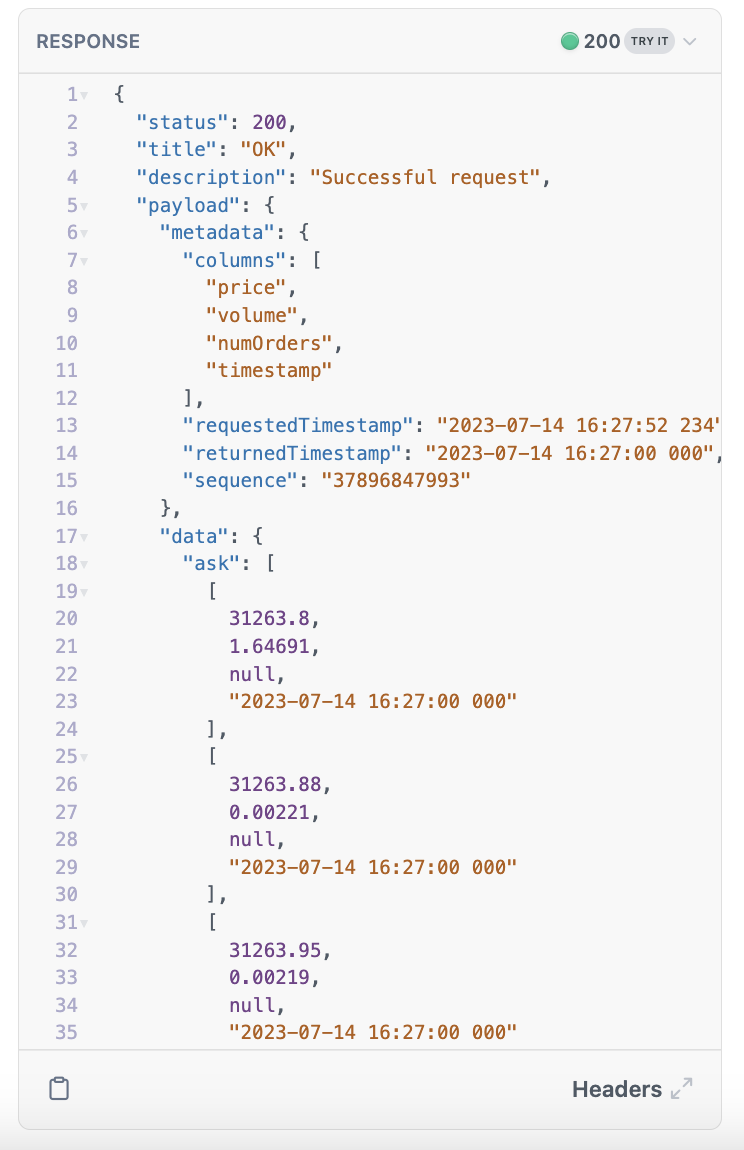

Binance Order Books

Our API supports full Binance order books which allow you to see every bid and ask for every asset and pair on every exchange we support. If you need to reconstruct an order book from Binance, with a particular pair from a particular point in time, you can do this from our REST endpoints. This is particularly useful if you are doing research, backtesting a model or just want to see what happened in the past with a particular dataset.

We offer order book data across all four of our market data sections: spot, swaps, futures and options. In addition to the full order book, we also have snapshots of the order books for the same four sections. These snapshots are 1-minute looks at the order books. If you don’t need the deepest granularity of the full order book, the snapshot endpoints are the next best thing and enable you to see what happened at a higher level for any pair at any time on Binance.

- Bid: the highest rate that someone is willing to buy the currency from you

- Ask: the lowest rate that someone in the market is willing to sell you the currency

- Mid: the average of the bid and ask rates (the bid and ask prices will be either side of the mid-market rate)

- Last: the price at which the last trade occurred

We offer Order book snapshots and order book events with granularity from one minute to one day. Order book events with every latest order book bid and ask on Binance. Our order book data is extremely granular and includes every ‘flick’ of a bid or ask for any pair on Binance.

We collect Order Book Snapshots via Binance’s REST API: the snapshot is a one minute snapshot. Every minute we get the full order book, full depth, as much as Binance provides. We offer real-time streaming order book data via Websocket subscriptions for all four order book types; spot, options, futures and swaps. We also offer FIX protocol. We get our order book data directly from Binance.

Our Order Book endpoints are available via REST API for latest and historical (time series) data as well as WebSockets for real-time data and AWS S3 for futures.

Here is a sample file.

Binance Order Books API Endpoints

Spot

/market/spot/order-book-events/{pair}/historical

/market/spot/order-book-snapshots/{pair}/historical

/market/spot/order-book-snapshots/information

Futures

/market/futures/order-book-events/information

/market/futures/order-book-events/{instrument}/historical

/market/futures/order-book-snapshots/information

/market/futures/order-book-snapshots/{instrument}/historical

Options

/market/options/order-book-events/information

/market/options/order-book-events/{instrument}/historical

/market/options/order-book-snapshots/information

/market/options/order-book-snapshots/{instrument}/historical

Swaps

/market/swaps/order-book-events/information

/market/swaps/order-book-events/{instrument}/historical

/market/swaps/order-book-snapshots/information

/market/swaps/order-book-snapshots/{instrument}/historical

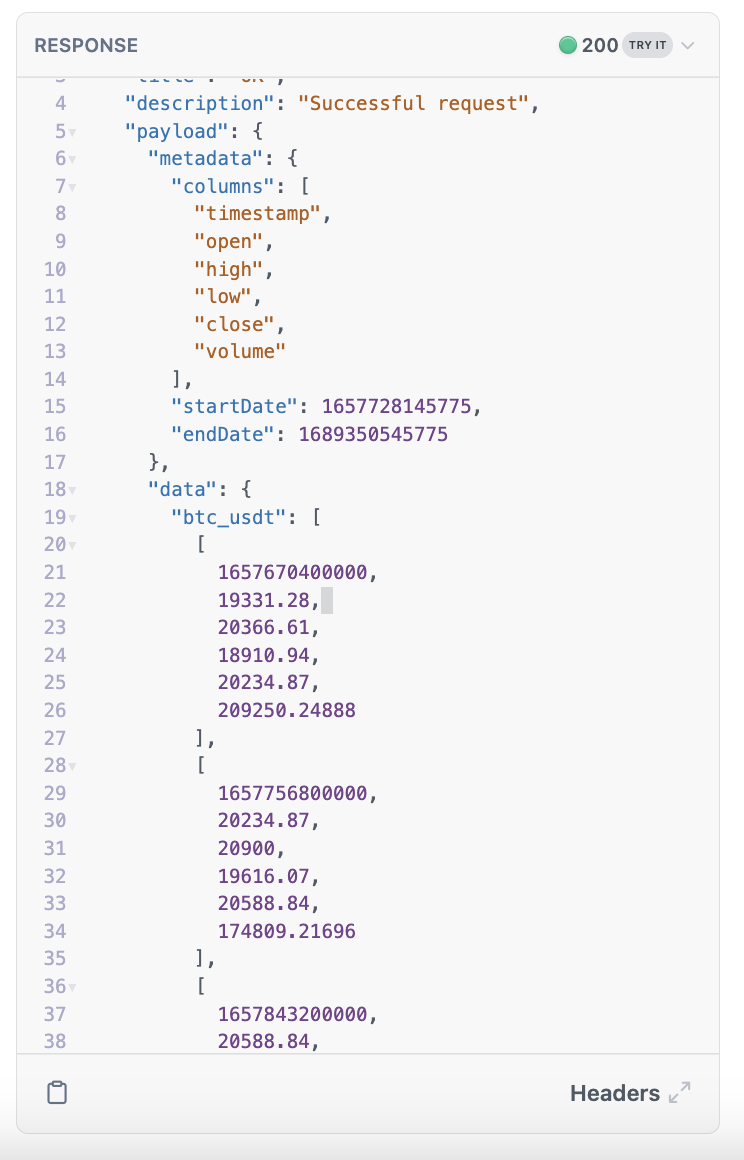

Binance Historical OLHCV Data

OHLCV is an aggregated form of market data standing for Open, High, Low, Close and Volume. OHLCV data includes 5 data points: the Open and Close represent the first and the last price level during a specified interval; High and Low represent the highest and lowest reached price during that interval; Volume is the total amount traded during that period. This data is most frequently represented in a candlestick chart, which allows traders to perform technical analysis on intraday values. Binance computes its daily candles at 00:00:00.

Our spot data for Binance goes back to 2017-08-17 and for Binance futures to 2019-09-08. We do not cover Binance US. For the OHLCV values, the price is always in quote and the volume unit is always in base. For example, if the pair was BTC-USD, then the price values returned are in USD and the volume value is in BTC. Our OHLCV endpoints are available via REST API for historical (time series) data as well as WebSockets for real-time data.

Here is a sample file.

Binance OHLCV API Endpoints

Spot

/market/spot/ohlcv/information

/market/spot/ohlcv/{pair}/latest

/market/spot/ohlcv/{exchange}/exchange/latest

/market/spot/ohlcv/{pair}/historical

/market/spot/ohlcv/{exchange}/exchange/historical

Futures

/market/futures/ohlcv/information

/market/futures/ohlcv/{instrument}/latest

/market/futures/ohlcv/exchange/{exchange}/latest

/market/futures/ohlcv/{instrument}/historical

/market/futures/ohlcv/exchange/{exchange}/historical

Options

/market/options/ohlcv/information

/market/options/ohlcv/{instrument}/latest

/market/options/ohlcv/exchange/{exchange}/latest

/market/options/ohlcv/{instrument}/historical

/market/options/ohlcv/exchange/{exchange}/historical

Swaps

/market/swaps/ohlcv/information

/market/swaps/ohlcv/{instrument}/latest

/market/swaps/ohlcv/exchange/{exchange}/latest

/market/swaps/ohlcv/{instrument}/historical

/market/swaps/ohlcv/exchange/{exchange}/historical

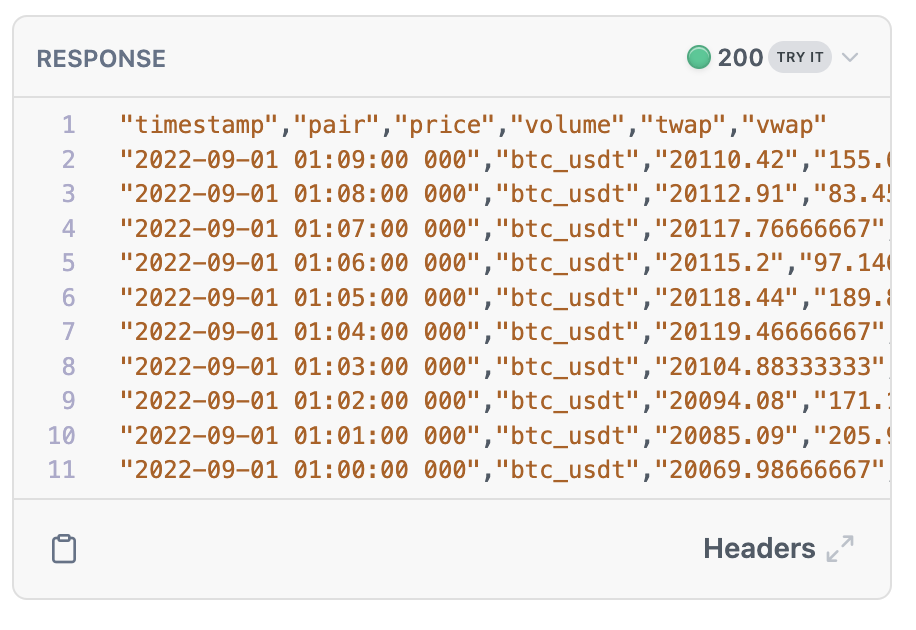

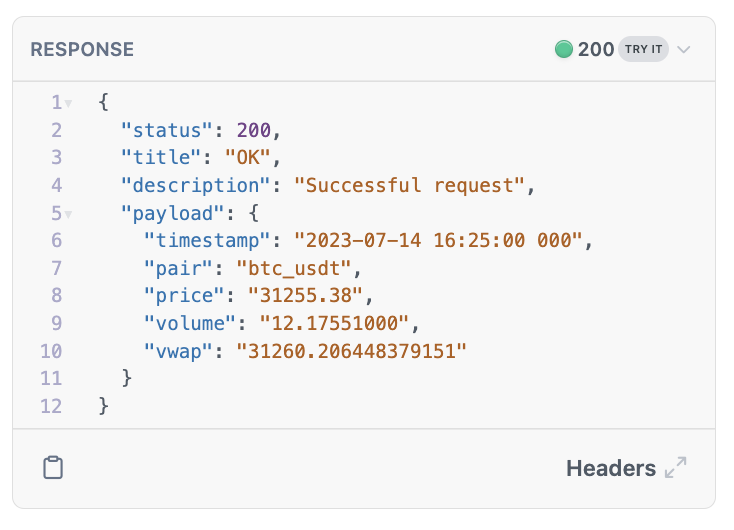

Binance Historical VWAP Data

For Binance, we provide VWAP data aggregated minutely, hourly, or daily, with historical data back to 2017-08-17. We calculate VWAP weighted by volume with a one minute frequency and a configurable lookback period. It is derived from the OHLCV data with the following calculation: (H+L+C) / 3.

Our VWAP data is available via REST API for historical (time series) data as well as WebSockets for real-time data.

Here is a sample file.

Binance VWAP API Endpoints

Spot

/market/spot/vwap/assets/information

/market/spot/vwap/assets/{asset}/latest

/market/spot/vwap/assets/{asset}/historical

/market/spot/vwap/pairs/information

/market/spot/vwap/pairs/{pair}/latest

/market/spot/vwap/pairs/{pair}/historical

Binance Historical Ticker Data

We provide Historical and live best bid and best ask (top of the books) for any traded instrument, as well as incremental tick-level updates/deltas of all bids and asks on an order book. This level 2 data is available within the Order Book endpoints. From this tick-level order book data, we are able to derive Tickers, which is simply the best bid and best ask (top of the order books) for a traded instrument.

Our spot data for Binance goes back to 2017-08-17; for Binance futures, 2021-04-12; and for Binance.US spot, 2022-06-15.

Our Tickers endpoints are available via REST API for historical (time series) data as well as WebSockets for real-time data.

Here is a sample file.

Binance Tickers API Endpoints:

Spot

/market/spot/tickers/information

/market/spot/tickers/{pair}/latest

/market/spot/tickers/{pair}/historical

Futures

/market/futures/tickers/information

/market/futures/tickers/{instrument}/latest

/market/futures/tickers/{instrument}/historical

Options

/market/options/tickers/information

/market/options/tickers/{instrument}/latest

/market/options/tickers/{instrument}/historical

Swaps

/market/swaps/tickers/information

/market/swaps/tickers/{instrument}/latest

/market/swaps/tickers/{instrument}/historical

Binance Data Delivery & Partnerships

Amberdata’s Binance datasets can be accessed via multiple delivery channels, such as REST APIs, Snowflake, Google Cloud’s Analytics Hub, and Databricks. These methods ensure smooth integration of Binance market data into users' trading strategies, analytics, and research processes. The available datasets include:

- Order Book Snapshots

- Order Book Events

- Tickers

- Trade Data

- OHLCV

Explore Binance Data on AmberLens

AmberLens offers interactive dashboards featuring comprehensive Binance data, providing users with valuable insights into market trends, trading volumes, and price movements. These dashboards enable real-time analysis and visualization of Binance's market data, supporting traders and analysts in making informed decisions.

Users can explore detailed metrics and historical data through user-friendly interfaces, enhancing their understanding of market dynamics.

Get started with Binance data in AmberLens today.